Introduction

Last reviewed: May 2026. The regulatory framework (FSRA, DFSA), fee structures, and fiduciary criteria below are evergreen, but always verify a firm’s current licence and fee schedule directly before signing anything.

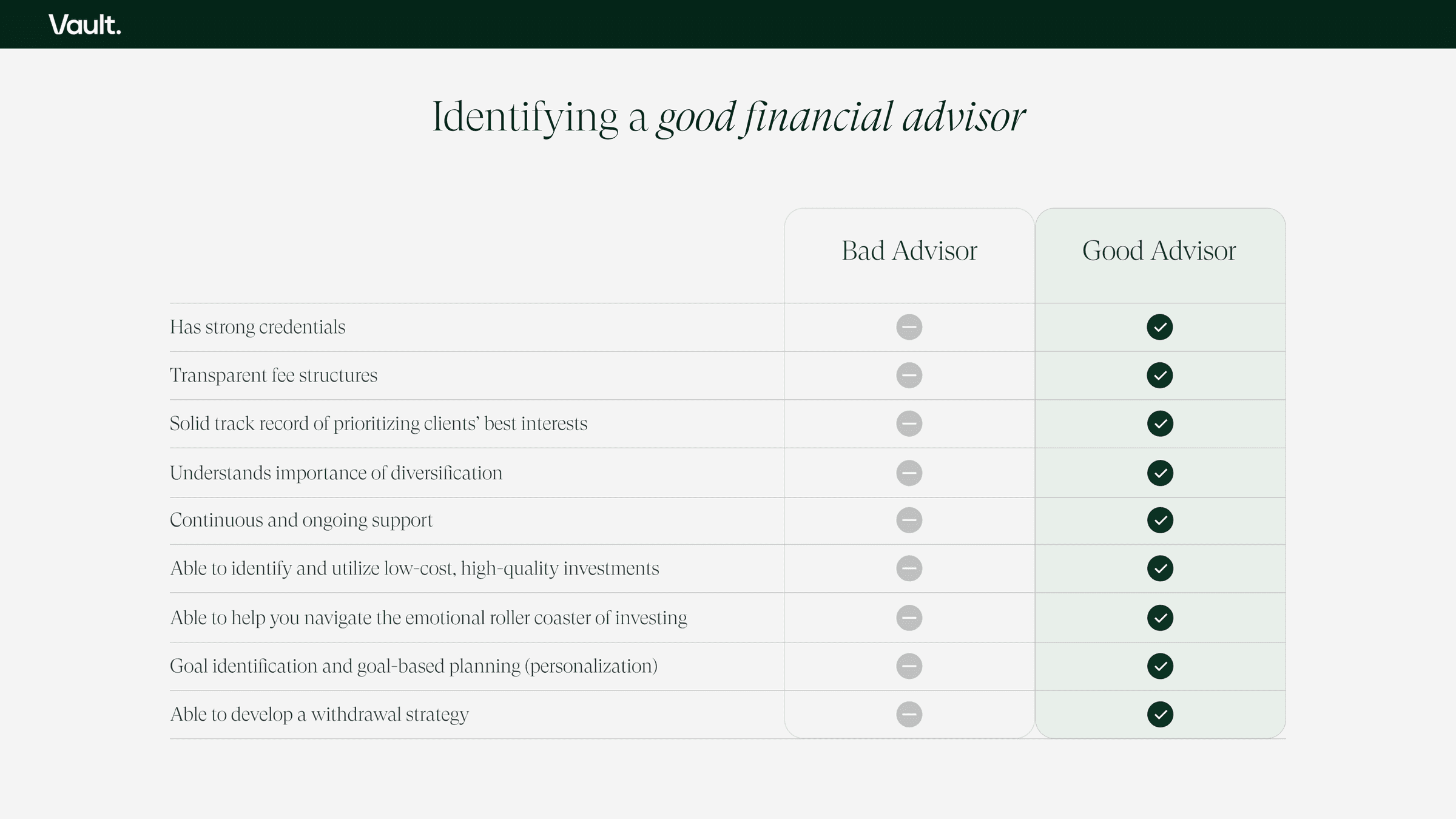

In a world of ever-changing financial markets and evolving personal circumstances, a good financial advisor can be an invaluable partner in helping you achieve your financial goals. By focusing on areas within their control, such as asset allocation, cost-effective implementation, and tax-efficient investing, they can add significant value to your wealth management strategy. Moreover, their expertise in behavioral coaching and retirement withdrawal strategies can lead to better long-term outcomes and peace of mind.

Choosing a financial advisor in Dubai & UAE

When considering a financial advisor in Dubai & UAE, there are several things to consider. For starters, from a cost perspective, a good financial advisor shouldn’t cost you anywhere more than 1% per annum. Furthermore, you need to ensure that you’re working with a true fiduciary; advisors who have a regulatory requirement to prioritize your best interests and are also incentivized by it, not by commissions. Another key consideration is their regulatory framework. The most stringent regulators in the UAE are ADGM’s FSRA and DIFC’s DFSA. Lastly, the more transparent they are, the less likely they are to be a shark. The UAE is unfortunately plagued by inconsistent advice, mis-selling of financial products, and lack of lasting relationships, all thanks to a swamp of bad actors or better yet, sharks. Last but not least, ensure you get their fees in writing.

Comparison of Financial Advisors in Dubai & UAE (2024)

Holborn Assets

- Regulating body - Not mentioned on website

- Fees - Not mentioned on website

- Assets under management - Not mentioned on website

- Digital platform - No

- Min. investment - Not mentioned on website

Finsbury Associates

- Regulating body - SCA UAE

- Fees - Not mentioned on website

- Assets under management - Not mentioned on website

- Digital platform - No

- Min. investment - Not mentioned on website

Vault

- Regulating body - ADGM’s FSRA

- Fees - 0.7% for $100K-500K, 0.4% for $500K-$5M, and bespoke for $5M upwards (No entry, exit, or product-based fees)

- Assets under management - Not mentioned on website

- Digital platform - Yes

- Min. investment - Exclusive to individuals with a min. $100K in liquid net worth

AES

- Regulating body - UAE Central Bank & DFSA

- Fees - Not mentioned on website

- Assets under management - Not mentioned on website

- Digital platform - No

- Min. investment - Not mentioned on website

DeVere

- Regulating body - UAE Central Bank

- Fees - Not mentioned on website

- Assets under management - Not mentioned on website

- Digital platform - No

- Min. investment - Not mentioned on website

Century financial

- Regulating body - SCA UAE

- Fees - Not mentioned on website

- Assets under management - Not mentioned on website

- Digital platform - No

- Min. investment - Not mentioned on website

Conclusion

We can’t overstate how important it is to select a financial advisor who is competent, ethical, and truly focused on your needs. A poor choice can lead to mis-selling, where advisors prioritize their commissions over your own best interest, resulting in potentially significant financial losses. This issue has plagued regions like the UAE, where many individual investors have lost confidence in the financial advisory industry due to the prevalence of unscrupulous practices and unaligned incentives. A prime example of this is the widespread promotion of ‘Whole of Life Insurance’ in the UAE, where the advisory firm makes a heavy upfront fee from the insurer to conduct the sale. In a majority of cases the policies are sold to clients seeking investments for their long-term future rather than an insurance policy

Disclaimer: The comparisons and evaluations made in this article are based on information gathered from the public campaigns and available data of the competitor products as of the time of writing. While we strive to provide accurate and up-to-date information, we do not represent, warrant, or assert the completeness or accuracy of the data. Our insights and comparisons are made to the best of our knowledge and are not intended to speak on behalf of any company’s offering or to disparage any company’s reputation.

Please note that this article is provided for informational purposes only and should not be construed as solicitation, investment, legal, or financial advice. Readers are encouraged to conduct their own research and due diligence or consult with a professional advisor for specific advice tailored to their situation. We accept no liability for any direct or indirect loss or damage arising from any inaccuracies, omissions, or the use of information contained in this article.

Frequently asked questions

How do I find a trustworthy advisor in the UAE?

Start with the regulator's public register: FSRA (fsra.adgm.com) for ADGM firms, DFSA (dfsa.ae) for DIFC firms, SCA (sca.gov.ae) for onshore-UAE firms. Then verify compensation model (must be fee-only), client references, and custody arrangements.What does "fiduciary" mean in the UAE context?

A fiduciary is legally and ethically bound to put your interests first. In practice that means: no commissions from product providers, transparent fee disclosure, and an advice process that's structurally aligned with your outcomes rather than the firm's revenue.Why is portable custody important?

Because your wealth shouldn't depend on any single firm's continued existence or your continued relationship with them. Assets held in your own name at a global custodian (e.g. Interactive Brokers) can be moved to another advisor — or self-managed — without forced liquidation.Are the larger banks "safer" choices?

Size doesn't equal safety on the advice-quality dimension. Large private banks have well-developed institutional processes but often operate commission-driven sales models that misalign incentives. The right test is fiduciary structure, not brand recognition.

Related reading

More on UAE & GCC

- InsightWealth Planning & Family-Office Architecture for Emirati Families: A 2026 GuideA practical wealth-planning and family-office guide for high-net-worth Emirati nationals — multi-generational continuity, concentration management, DIFC/ADGM foundation architecture, Sharia-compliant succession, and the operational discipline of an institutional-grade family office.

- InsightWealth Planning for HNW Bahraini Expats in the UAE: A 2026 GuideA practical wealth-planning guide for high-net-worth Bahraini nationals managing wealth across Bahrain and the UAE — GCC mobility, regional banking depth, family-business succession, and DIFC/ADGM structuring.

- InsightWealth Planning for HNW Belgian Expats in the UAE: A 2026 GuideA practical wealth-planning guide for high-net-worth Belgian expats in the UAE — Belgian tax residency, the new capital-gains regime, the Cayman tax, regional inheritance rates, and the Belgium-UAE DTAA.