Introduction: Negative Sentiment

Over the past year, financial news has been dominated by negative sentiment, particularly when it comes to earnings.

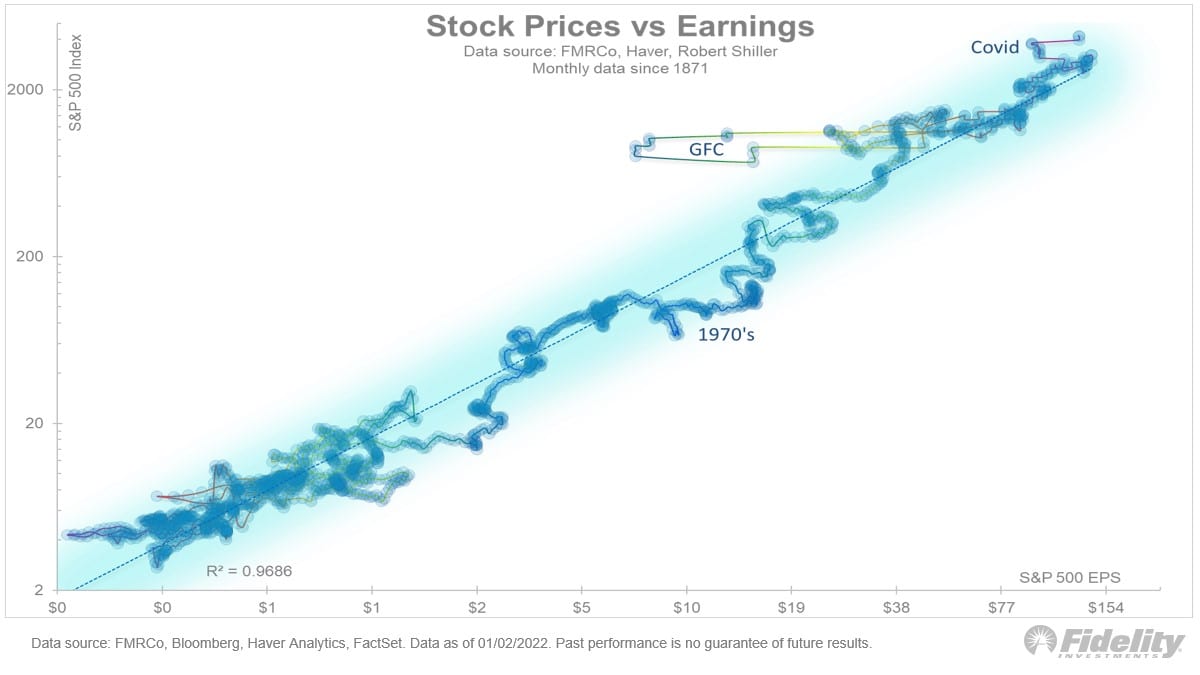

No doubt, corporate earnings stand as the best barometer for company valuations (and hence, equity market performance). Below is an excellent chart portraying just how strong this correlation is, showing how the core driving factor of a company's valuation is the annual earnings it generates.

Source: Jurrien Timmer - Fidelity

This relationship has kept many investors feeling very uneasy due to continuous predictions of an impending earnings recession, a prospect that's been on the horizon since last year.

The question then must be asked, "why has the equity market performance been this positive in the past months despite these predictions?"

We must remember that equities represent owning actual companies, and no one buys a company for its cash flows for that precise year. When we choose to own a company, we do so by anticipating its earnings over multiple years to come. And therefore, the chart we referenced above shows that earnings are the most important driver of equity performance only in the long run, but has no predicting power in the short run. Especially because the equity markets are forward-looking, which means most predictions on earnings are well priced-in before the event occurs. What usually really hurts equities is a non-projected earnings drop which has the potential of continually hampering earnings for years to come. That's why markets were so worried at the onset of the virality of COVID, as there was an unpredictability on what was to come.

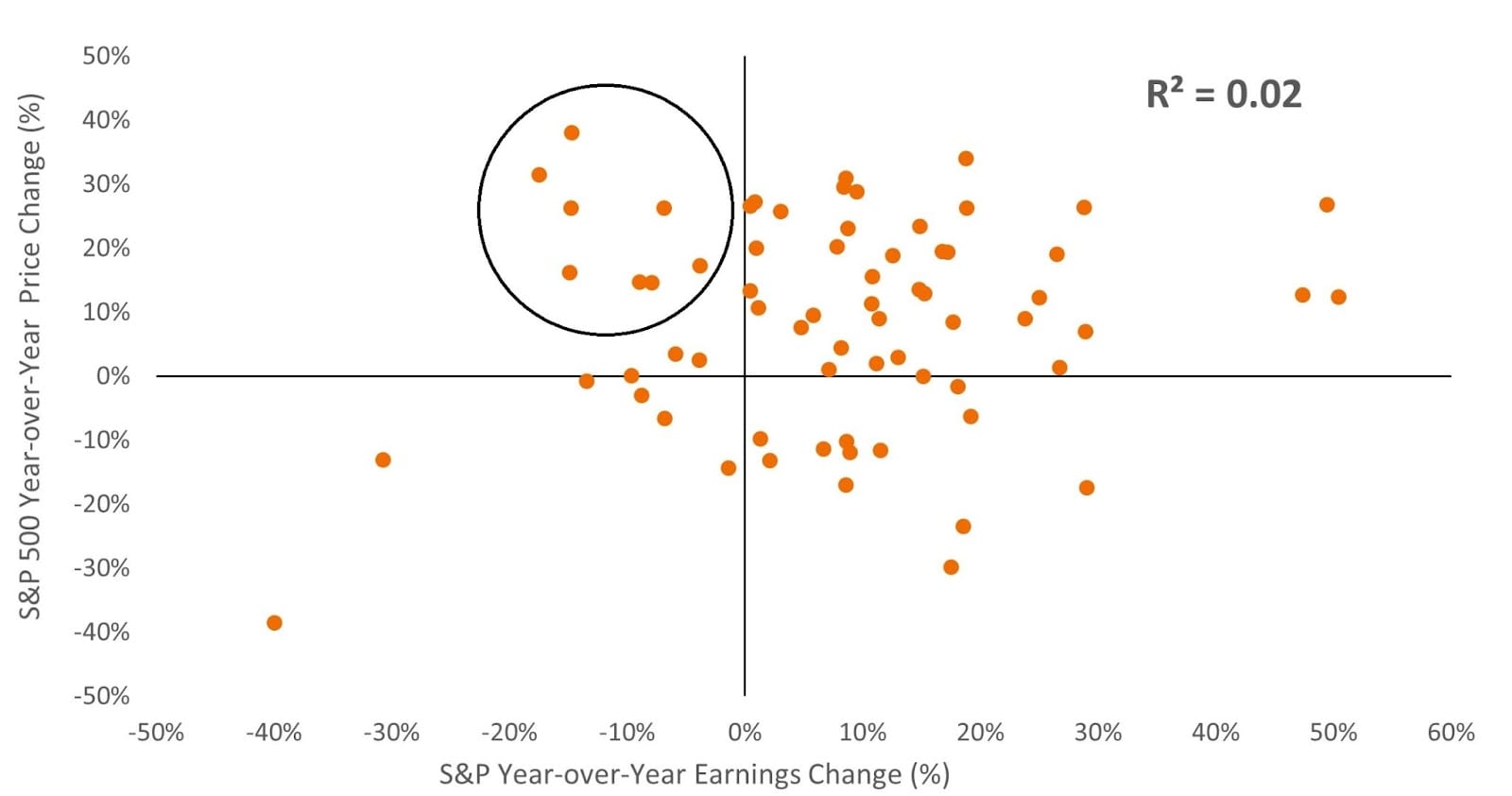

The best way to exhibit this is to look at another dot-plot chart showing all years since 1955 to 2022:

Source: Bloomberg, NYU Stern/Prof. Damodaran, as of 2 December 2022. S&P 500 Index price and earnings series from 1955 to 2022. All data points shown are for December 31 of each year, except for 2022 which is December 2 data. No transaction costs. R2 shown is the coefficient of determination between year-over-year changes in annual earnings and the S&P 500 Index; a value close to zero suggests that one-year earnings changes are not a good predictor of one-year stock price changes. Past performance does not predict future returns.

In the chart above, we see the top-left quadrant showing years where earnings were negative year-on-year, but equity performance was strongly positive. This historical data proves that negative earnings growth does not suggest an equity market decline whatsoever.

So when market commentators continue to project a gloomy outlook to capture screen time, remember that they're most often mistaken.

Conclusion

In terms of bonds, despite the positive performance of equity markets in the recent past, there's been no significant revision in bond prices. This stagnancy is largely due to continued positive economic data, which keeps pushing potential interest rate drops further into the future. Nevertheless, the current investment climate presents an opportunity to lock in relatively higher interest rates for longer periods than previously possible. If an unforeseen, sustained earnings decline were to occur, one can reasonably expect one of the first policy responses to be a drop in interest rates, which would prove highly beneficial for bonds. Meanwhile, the possibility of a significant interest rate surge from this point seems exceedingly unlikely, thereby limiting the downside of such a balanced investment strategy.

Frequently asked questions

What is an "earnings recession"?

Two or more consecutive quarters of declining aggregate corporate earnings — distinct from an economic recession (negative GDP). Predicted earnings recessions don't always coincide with predicted economic recessions, and neither prediction is reliably accurate.Why did the predicted earnings recession not materialise?

Aggregate earnings proved more resilient than forecasters expected. Specific sectors did contract — particularly rate-sensitive sectors and pre-pandemic-pull-forward beneficiaries — but other sectors (technology, energy, healthcare) compensated. The aggregate stayed approximately flat to slightly up.What's the lesson for investors?

Don't position the whole portfolio for any single forecast. Forecasts about aggregates frequently miss the sectoral dispersion that ultimately determines outcomes. Diversified investors capture the resilient sectors automatically; concentrated investors positioning for the predicted scenario often miss the actual one.

Related reading

More on Markets & macro

- NewsletterWhat 2025’s Market Turbulence Is Teaching InvestorsResearch shows that investor behaviour — staying invested, rebalancing, avoiding reactive decisions — has more impact on outcomes than any single market call.

- NewsletterGold’s Surge and What It Could Mean for InvestorsGold prices are soaring to record highs, but is the rally sustainable? Explore what’s driving demand, the risks ahead, and gold’s role in a modern portfolio.

- NewsletterIs the AI Boom a Bubble, or Just the Beginning?AI valuations are soaring — but is it sustainable? Discover what's fuelling the hype, where risks lie, and how MENA investors can stay exposed and protected.